Could 2021 be the “Perfect Storm” for US Cattle Producers?

By Ralph Godsey

This blog originally appeared on the Data Sway blog.

As anybody in the cattle and hay industry already knows 2021 has been a tough year and potentially could get tougher. The contributing factors are: the drought conditions that lead to a decreased hay production, the quantity of quality hay exports, and a bottleneck in the cattle supply chain. The question is could these factors be setting up US cattle producers for a “Perfect storm” situation?

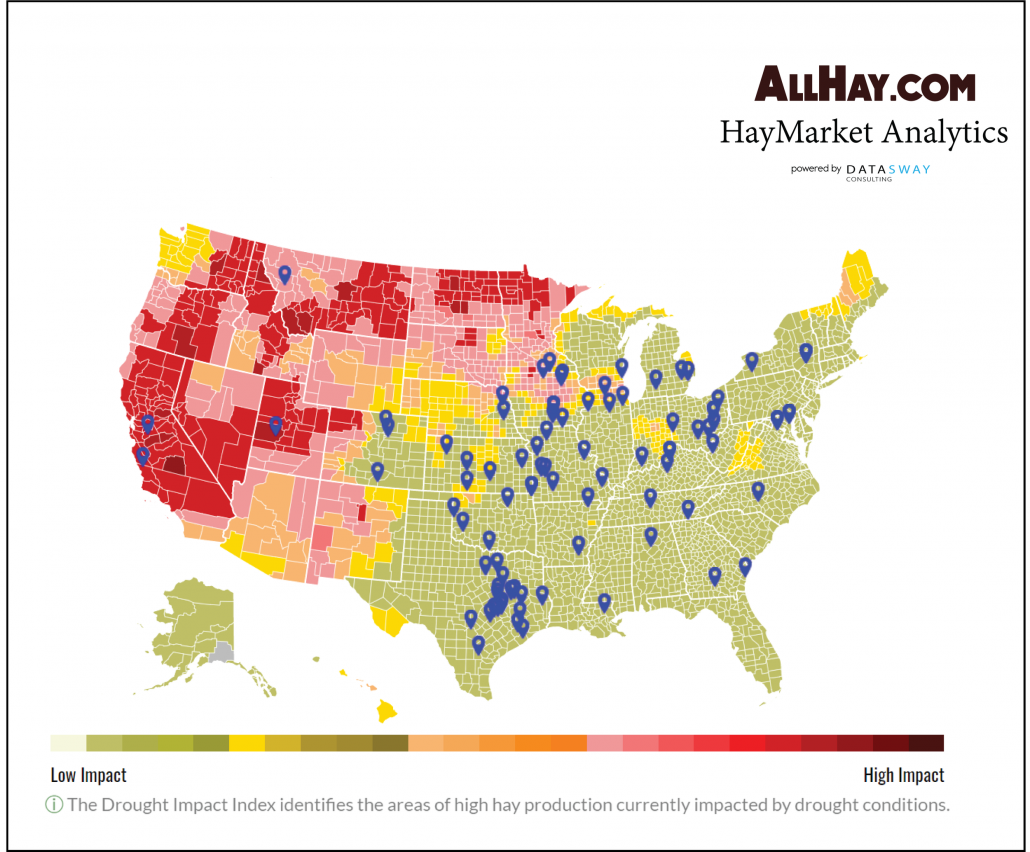

This years drought conditions have been the worst in recorded history for hay production. This has had adverse effects and not just for the West Coast hay producers; on which it has been devastating.

This spring it was estimated that the total US hay stockpiles we’re down 12% from the same time the previous year.

In addition to rainfall many hay producers in the Northwest and West rely heavily upon irrigation for their water supply. In May some of the reservoirs, which are critical supply resources for irrigation, we’re measuring 15% lower than average. Expectations were that these systems might only receive 25% of the addition water accumulation that they would otherwise expect for the year. The dry soil conditions in the mountainous areas severely handicapped the potential for reservoir resupply. This occurs when snowpack runoff cannot not reach the basins because it is absorbed by the soil before ever having a chance to make its way into these systems. As a direct result of this, current hay production losses in North Dakota, Montana, and Washington alone have been estimated to be 35% and equate to approximately 3.2M tons less than 2020.

Despite an increase in late season rainfall in the Great Plains states, supplemental feeding has been a necessity for many in this region. Estimates are showing that greater than 60% of the Great Plains ranchers are already introducing supplemental hay regiments.

According to the USDA’s National Agricultural Statistics Service (NASS) in July, total alfalfa production for 2021 was down nearly 10% representing an acreage loss of about 100,000 and other hay production was estimated to be down 2.5% or 600,000 fewer acres. These conditions alone have made all classes of hay more expensive in every region and forced many ranchers to start feeding sooner, when they would otherwise be grazing herds in lush green pastures.

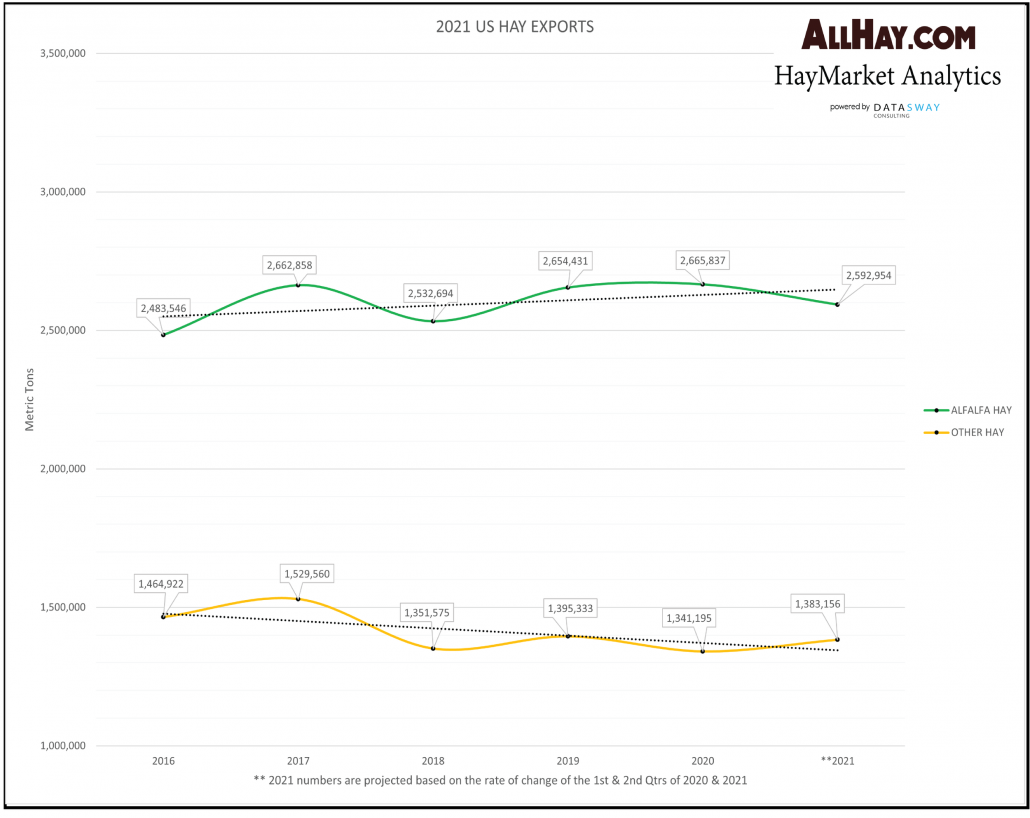

Exports of premium quality hay

Despite the extreme drought conditions inflicted upon many US hay producers and the resulting production losses, total US hay exports are projected to only marginally decrease by only 0.7% this year.

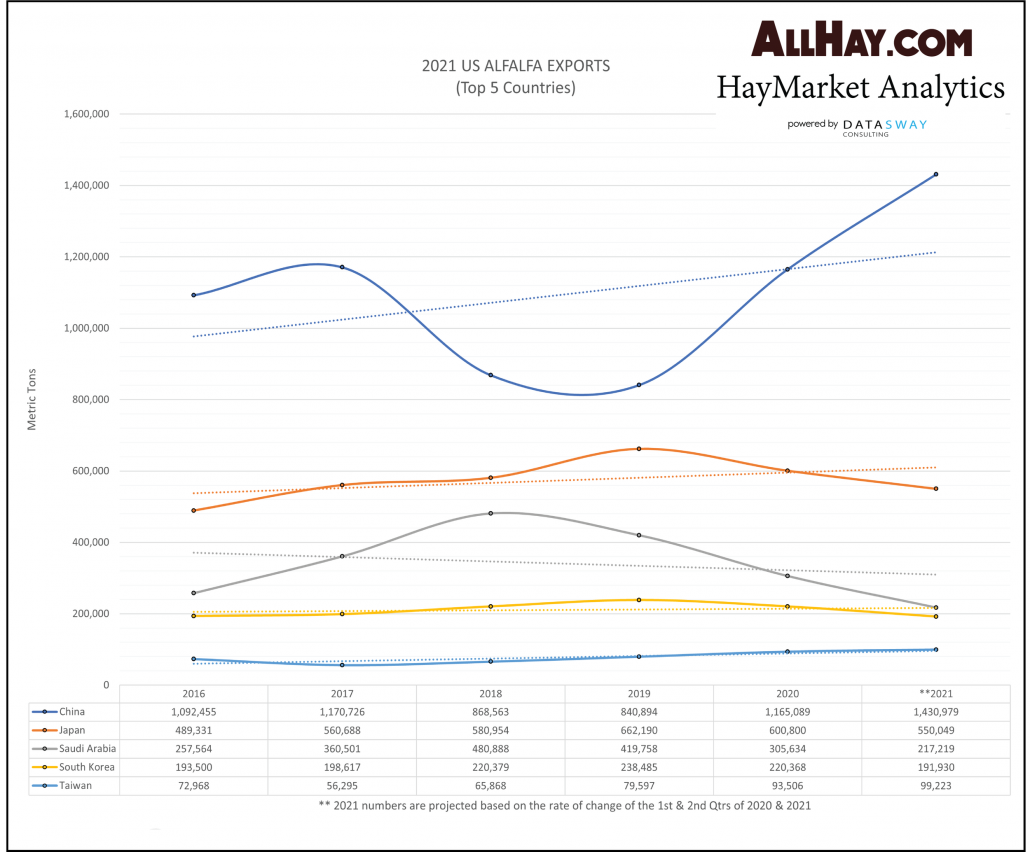

It is interesting to note that China has stepped up their exportation of high-quality alfalfa hay by 22.8% in just the first half of this year. In 2020 China exported nearly 1.2 million metric tons of alfalfa and this year, if exportation rates continue through to December, they’re on track to exceed 1.4 million metric tons. This is approximately 35.2% more than the four other top US alfalfa exporters (Japan, Saudi Arabia, South Korea, and Taiwan) combined.

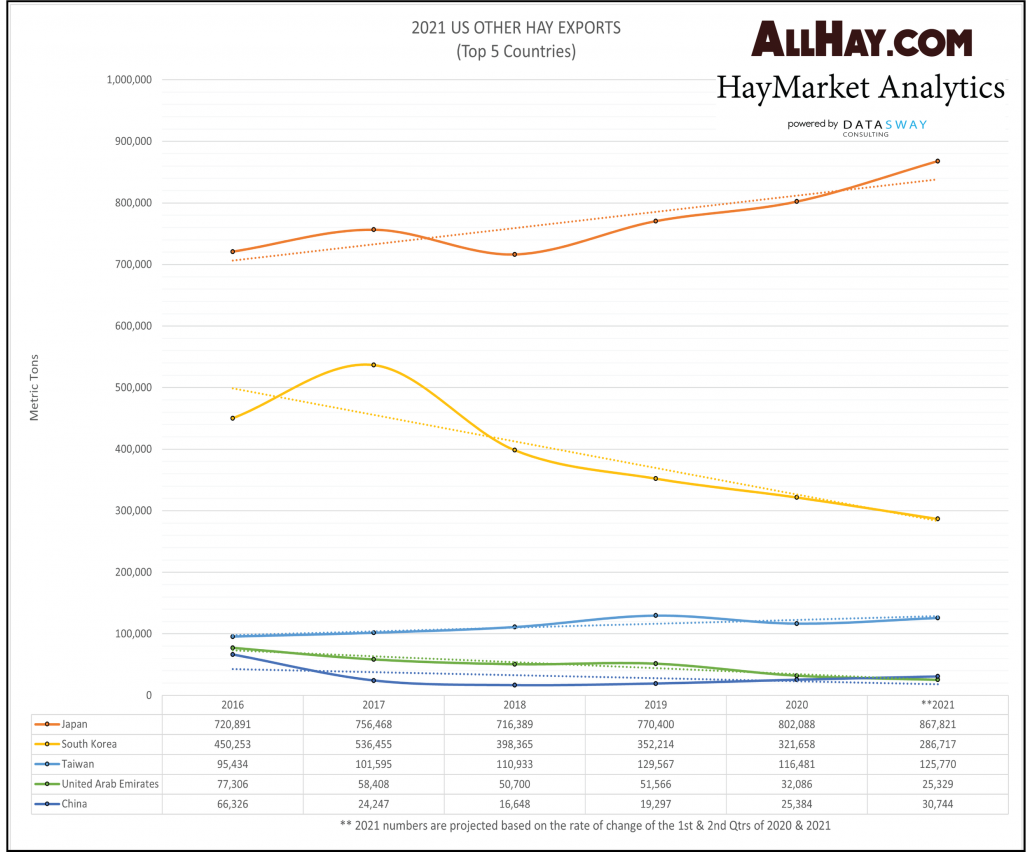

Additionally, their exports of “Other hay” from the US has increased by 21.1%. With US stockpiles of hay already at incredible lows where does this leave the US cattle producer? In competition for vital resources that’s where and market hay prices driven sky high, with no end in sight for the foreseeable future.

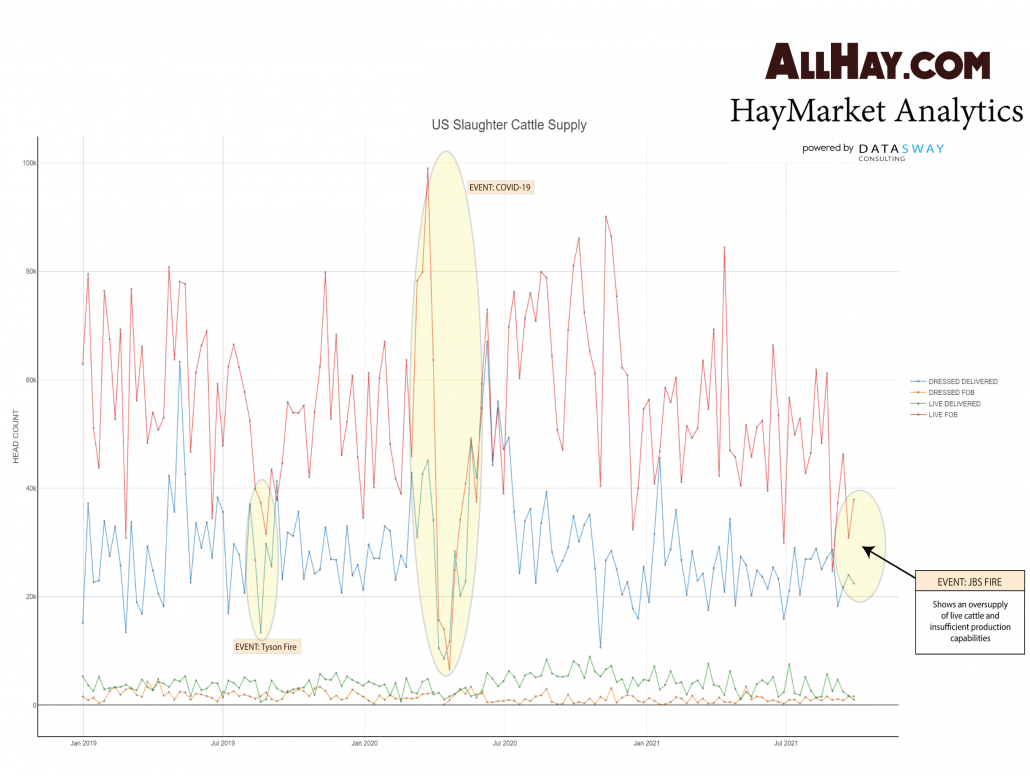

Slaughter cattle production drop-off

The September 13th JBS fire has sent shockwaves through both feeder cattle markets and that of slaughter cattle. With this 6% reduction of US processing capacity, we are seeing feedlots dealing with an oversupply issue and a processing underproduction issue on the slaughter side. To compound the problem feed lots and slaughterhouses still have not fully recovered from the labor shortage brought on by COVID-19. Prior to this fire many live cattle markets were experiencing an uptick in sales partly because of the good heifer and steer prices but also because ranchers have seen the writing on the wall and are selling in anticipation of low hay stocks this winter.

Conclusion

These events if taken separately may be of little or no consequence.. However together they have an additive effect and create the potential for a “Perfect storm” in the US cattle industry. This may cause many small and medium cattle producers severe and painful economic problems in the coming months. Situational awareness is the key to survivability. Cattle producers must take actions now to avoid herd liquidations and harsh economic losses resulting from not being able to feed this winter. The best medium to do this is to acquire a stockpile of quality feed materials now while you can and if you can afford it.